In the modern economic landscape, interest rates are the silent engine driving every financial decision. Most consumers view interest simply as a percentage attached to their monthly statements, but its influence runs much deeper. Interest is essentially the rental cost of capital; it represents the fee you pay to access money today that you haven’t yet earned. Understanding the granular details of how these rates are calculated, adjusted, and applied can be the difference between achieving financial freedom and falling into a permanent cycle of debt. To truly master your finances, you must look beyond the surface and analyze how the “price of money” dictates the trajectory of your personal wealth.

The Macro View: Where Do Rates Come From?

Interest rates do not emerge from a vacuum. They are primarily influenced by the monetary policy of a nation’s central bank. When a central bank raises its benchmark rate to combat inflation, it becomes more expensive for commercial banks to borrow money. These banks then pass that cost down to you. This is why you might notice that your credit card APR or mortgage offer increases shortly after a government announcement. However, the market rate is only the starting point. Your personal rate is determined by your “Risk Profile,” which lenders evaluate through your credit score, income stability, and existing debt levels.

The Mechanics of Amortized Loans

For major purchases like homes and vehicles, interest is applied through a process called amortization. This is a structured repayment schedule where each payment is split between the principal amount and the interest. In the initial phase of a long-term loan, such as a 30-year mortgage, a disproportionate amount of your monthly payment goes toward interest. This means that for the first several years, you are barely reducing the actual debt you owe; you are primarily paying the bank for the privilege of the loan. As the loan matures, the ratio shifts, and more of your money begins to chip away at the principal. This structure is why even a 0.5% difference in your interest rate can result in tens of thousands of dollars in extra costs over decades.

Fixed vs. Floating: The Strategy of Choice

Choosing the right interest structure is a critical strategic move. Fixed-rate loans offer the luxury of predictability; your payment remains constant regardless of economic turmoil. This is ideal during periods of historically low rates. On the other hand, floating or variable rates are tied to market indices. While they often start lower than fixed rates, they carry the risk of “payment shock.” If global interest rates rise, your monthly obligation follows suit, which can quickly destabilize a household budget. Successful borrowers often weigh their tolerance for risk against the current economic climate before committing to one or the other.

The Hidden Trap of Credit Card Interest

While mortgages are predictable, credit cards are dynamic and potentially dangerous due to how they calculate interest. Unlike standard loans, credit cards often use “daily compounding.” This means the issuer calculates interest on your balance every single day. If you carry a balance from month to month, you aren’t just paying interest on your purchases; you are paying interest on the interest accrued the day before. This mathematical phenomenon can cause debt to grow exponentially, far outpacing a consumer’s ability to pay it off. This is why high-interest credit card debt is often cited as the number one obstacle to building long-term savings.

According to Investopedia, credit card interest is commonly compounded daily, meaning interest is charged on both the principal balance and previously accrued interest, which can accelerate debt growth significantly.

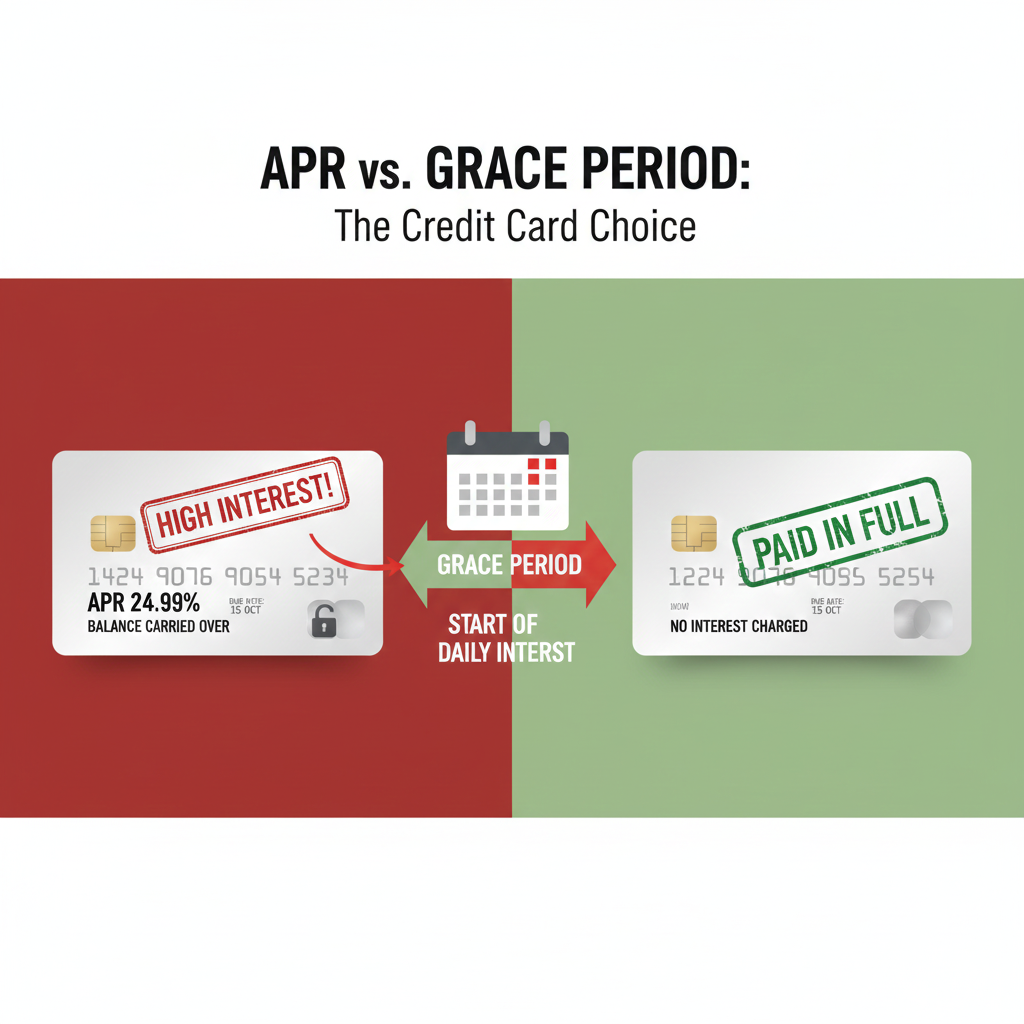

The APR vs. the Grace Period

Many consumers focus on the Annual Percentage Rate (APR), but the most important feature of a credit card is actually the “grace period.” Most cards offer a window of 21 to 25 days where no interest is charged if the statement balance is paid in full. Once you carry over even a small fraction of that balance, the grace period vanishes for all subsequent purchases. Suddenly, every cup of coffee or grocery trip begins accruing high-interest charges from the moment of purchase. This shift transforms a convenient payment tool into an expensive high-interest loan. Understanding this “all-or-nothing” nature of credit card interest is vital for maintaining a healthy financial status.

The Psychology of Interest and Minimum Payments

Lenders often set minimum payments at a very low level, usually just enough to cover the interest and a tiny fraction of the principal. This is a deliberate strategy to keep the borrower in a “revolving” state. When interest rates are high—often exceeding 20% on many cards—making only the minimum payment ensures that the debt will take decades to satisfy. By the time the balance reaches zero, the borrower may have paid three or four times the original cost of the items purchased. Breaking this cycle requires a mindset shift: viewing credit card balances as emergencies that need to be extinguished immediately rather than manageable monthly costs.

Impact on Credit Utilization and Future Rates

Interest rates also have a secondary, indirect impact on your credit health. As interest accrues on unpaid balances, your “Credit Utilization Ratio” increases. This ratio—how much you owe compared to your total credit limit—is a massive factor in your credit score. When high interest causes your balances to creep upward, your credit score drops. This creates a “debt spiral” where you are then forced to accept even higher interest rates on future loans because you are now seen as a higher-risk borrower. Maintaining low balances is not just about saving on interest; it’s about protecting your access to affordable capital in the future.

Conclusion: Taking Control of the Cost of Time

Ultimately, interest is the price of time. High interest rates shorten your financial reach, while low rates expand it. To manage these costs effectively, you must be proactive. This includes regularly reviewing your accounts for better rate offers, utilizing balance transfers to move high-interest debt to 0% APR platforms, and always paying more than the minimum. By understanding that interest is a variable you can influence through your behavior and credit maintenance, you move from being a passive payer to an active manager of your financial destiny. Knowledge is the only tool that can truly neutralize the “invisible cost” of borrowing.